Medishield is a set of basic health insurance that is administered by the Central Provident Fund (CPF) Board. It helps to pay for large hospital bills and costly outpatient treatments, such as dialysis and chemotherapy for cancer.

The Government recently announced the introduction of Medishield Life in Nov 2015. Medishield Life, in short, is an upgraded version of Medishield. The key changes for Medishield Life are:

- Higher claim limit

- It covers pre-existing conditions

- Coverage is for life

These changes are in line with Medishield Life slogan: “Better protection. For all. For life”

Here are five things you need to know about Medishield Life

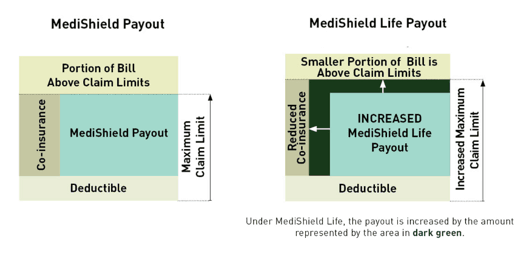

1. It provides better benefits than Medishield (Better Protection)

First of all, the hospitalization bill is divided into 3 portion. The first portion is what is known as Deductibles, which can range from $1500 to $3000 depending on which class of ward admitted to. This portion of hospitalisation bill is paid by you, even if you have Medishield or Medishield Life.

The second portion of hospitalisation bill is termed Co-insurance. For Medishield, co-insurance ranges from 10% to 20% of the total bill and for Medishield Life, co-insurance ranges from 3% to 10% of the total bill. This second portion of hospitalisation bill is also paid by you.

The third portion of the hospitalisation bill will be paid by Medishield or Medishield Life. Currently, the Medishield limit per year is $70,000 and $300,000 per claimant lifetime. In the future, the Medishield Life claim limit per year will be increased to $100,000. On top of that, the lifetime claim limit will also be removed. Below is the graphical presentation of hospitalisation bill by MOH.

2. It covers everyone (For All)

Currently, those who has pre-existing medical conditions are not covered under Medishield. In line with the principle of universal coverage, the new Medishield Life will cover all Singapore Citizens and Permanent Residents including those who have pre-existing conditions and who may not have been able to obtain insurance coverage. Their pre-existing conditions will also be covered. These people with pre-existing medical conditions may need to pay up to 30% additional premium for the coverage.

3. It protects you forever (For Life)

Current Medishield only covers up to age 92. Individuals who has longer life span will be unprotected after the age 92, when they need health insurance the most. Medishield Life, as the name implies, is for Life. You will get coverage for your entire life so there is one more reason to stay healthy and live longer 🙂

4. All premiums will be payable by medisave

With the increase in benefits, the Medishield Life premium will also be higher than Medishield.

However, the Government allows all premium for Medishield Life to be payable by Medisave. This means that you will not have to worry about coming up with more cash in order to pay for the better protection by Medishield Life.

5. No need to apply

Medishield Life will cover all Singaporeans and Singapore PRs from 1st of November 2015. There is no need to apply for Medishield life. You should receive a letter in September informing you of your premium payable for Medishield Life.

In Conclusion

Here are the summary of what you can expect from Medishield Life:

- Fully payable by Medisave Account

- Covers Pre-existing conditions

- Covers hospitalisation in Class B2/C wards in restructured hospitals

- Maximum Claim Limits: $100,000 per year

- Does not cover deductibles and co-insurance

- Overseas Medical Treatment is excluded

As you can see, while Medishield Life is a definite improvement over the current Medishield scheme, it is still not fully complete. You might still end up incurring a fair bit of out of pocket expenses. In my next article, we will discuss the Private Integrated Shield Plans and how they can supplement your Medishield Life coverage.

My colleague mentioned that with the cpf life, we basically will not see our cpf money if we die shortly after the start of the payout from cpf life.

He mentioned that at 55, you can take out the excess of your min. Sum. The min. Sum is then go to cpf life which is an annuity. The 1st premium is deducted @ 55 and the next deducted before start of payout which is today @ 65. @ 65 cpf life starts giving you monthly payouts. If you only enjoy say 2yrs of payout ie u die @ 67 the bal of your money in the cpf life gets into the common pool. It will not refund you the bal to give to your beneficiaries.

Is this comment correct?

Hi John,

Thank you for your comment. Your colleague is not entirely correct. Everything you mentioned is correct except that if you live until 67, the balance of your money in CPF life will be giving to your beneficiaries instead of gets into the common pool. Also, starting in 2016, government allows you to withdraw up to 20% of your CPF life at age 65. This is one of the new changes to CPF LIFE scheme.