All financial advisors have to go through the risk-profiling steps with their prospective clients. Typically, advisors will recommend bond funds for those risk-averse investors who want capital preservation. Similarly, bond funds are the default choice for investors in their retirement years, since they would not have enough time to recover from possible losses. Bonds are known to be capital guaranteed. This is a deadly belief without understanding how bond works. It might be detrimental advice to our elder folks and conservative investors at the current economic situation. I hope this article can explain the looming danger of this advice.

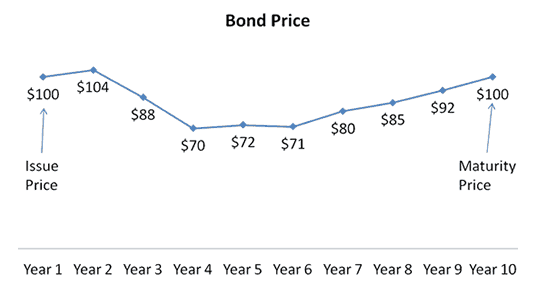

Bonds are only capital guaranteed at maturity

It is often mentioned that bonds are capital guaranteed. But they failed to add in a caveat – capital guaranteed at maturity ONLY. Bond price will fluctuate between issuance and maturity, as shown in the chart above. An investor who holds the bond till maturity will get back the capital, as well as all the coupon payments throughout the entire period. But if an investor sells before maturity, he can suffer a loss or make a profit, from the difference between the prevailing market price and his buying price.

Why does Bond Price move?

There are a few factors resulting in the changes in bond price. The main factor is interest rate movements. The other factors like Liquidity and Accrued Interest are small factors which can be ignored.

The bond coupon rate is closely linked to the interest rate at the point of issue. If interest rate is low, coupon rate is low too.

Let’s use an example to illustrate.

A bond was issued in 2013 with a coupon rate of 2.5% at $100. Let’s call this BOND A.

Assuming interest rate rises next year and another bond was issued in 2014 with a coupon rate of 5% at $100. Let’s call this BOND B.

New bond investors will prefer to buy BOND B because it has a higher coupon rate. In order to compete with BOND B, BOND A has to be sold at a lower price.

How much lower? BOND A should be sold at $50 in order to have the same bond yield of 5% as BOND B. In other words, the price of the bond dropped by 50%, from $100 to $50!

Hence, the important concept to grasp is interest rate and bond price are inversely related – interest rate goes up and bond price comes down, and vice versa.

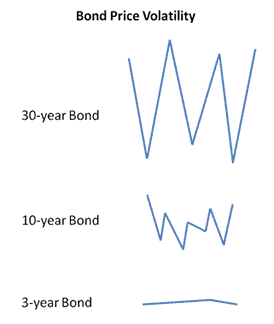

The longer to maturity, the higher the volatility

However, not all bond prices are so sensitive to interest rate changes. Short term bonds with 1 to 3 years to maturity are less volatile than long term bonds with 10 years or more to maturity. The diagram below illustrates the relationship between bond price and duration to maturity.

What can happen?

Interest rate has been kept low since the 2008 financial crisis. And this has fueled the the rise in bond prices.

On 18 Dec 13, the Fed commenced the tapering of bond buying, from $85 bn per month to $75 bn per month. Bernanke has also said it will be further reduced at a measured pace throughout 2014.

This means that interest rates are poised to rise in the coming years. And we learned earlier that rising interest rates means lower bond prices.

What should you do?

I mentioned that conventional risk profiling will recommend retirees and conservative investors to invest in bonds. This is definitely NOT A GOOD TIME TO INVEST IN BONDS. Bond investors could be in for a rude shock in the next few years when they realised their portfolio value has dropped significantly when the expectation was not to lose any money!

However, there are exceptions and it is alright to invest in bonds if

- You are happy with the coupon payments and do not intend to sell before maturity (assuming you are able to withstand the volatility)

- You buy a short term bond with maturity below 3 years (because short term bond prices are less sensitive to interest rate changes)

- You set up a portfolio diversified in different asset classes, e.g. Permanent Portfolio (yes, your bonds will still lose money, but some other assets are likely to make money and you can have opportunities to sell dear assets and buy cheap bonds)

Conventional risk profiling is ironically risky at this moment. Asking clients to buy bonds without considering the economic condition is doing more harm than good. I hope this article has helped you avoid a potential danger and save your hard earned money. Please do me a favour and send this warning to people you care about. They would thank you for it.

Then what would you suggest to a low risk investor?

Not all investors can appreciate the concept of permanent portfolio esp when gold just keeps falling down.

u r right that not everyone can appreciate PP.

not many people can stomach volatility too. even though that is a necessity for investment returns.

risk averse investors can have the following choices:

– fixed deposits

– short term bonds (mature less than 3 years)

– top up cpf account

Actually bond price falling does not necessary means that customer is losing money. For example bond price drop 10%. Yield to maturity is 8%. Customer actually starts to make money in the middle of 2nd year.

And corporate bond prices do not react to interest rate only, improve profitability of the companies can also help to push up bond price as well.

It isn’t wrong if he buys after the bond price drop. The yield is high only if the investor buy at lower bond price.

Corporate bond price will be affected if interest rates go higher than corporate bond coupon rates.

Without a doubt, there are more factors affecting corporate bond prices.

Hi Alvin,

I have a small doubt regarding the capital guarantee of bonds. In the e.g above, suppose one purchases the Bond in year 2 when it is at $104, at maturity, does he still get back $104 or does it drop to $100?

The investor only gets back the original price which the bond was issued. $100 in this case

hmm, so in that case, is it right to say that one was must be careful when buying bonds from the market when they are at a higher price. Or maybe, to put it in better words, one has to calculate the new bond yield (for e.g. if the coupon rate was 3%), the yield is now 3/104*100 = 2.88% and then compare it with other bonds before choosing the best bond to buy?

The bond yield example I used is a rough estimate. One should always use yield-to-maturity, which takes into consideration the age of the bond.

Sorry, I think I confused capital guarantee with yields with my comment above. Since the investor gets back $100 at maturity, capital is still guaranteed. The only loss is $4, which can probably be considered small in comparison to the return of 3$ per year that he will get, which is $27 if he holds until maturity. So net return = $27-4=$23, which is still not bad.

Am just still figuring out how these bonds work. Your site is really good! Keep up the good work 🙂

what if i do dollar cost averaging and invest a fixed amount in the bond monthly?

It will be better than investing lump sum now. But you need to invest for a long time and not give up when the bond price tanks.