Singtel, the once-upon-a-time telco monopoly, has garnered a respectable ~30% rally YTD after some positive news. We believe two key factors are fueling this rally.

Firstly, Singtel is showing very promising earnings growth, with increased profit for Q1 2025 compared to a huge profit drop in FY 2024. This signals an increase in the efficiency of the business. For a highly competitive telco industry in Singapore, this improvement in margins is critical to solidify Singtel’s dominance in the market.

Secondly, Singtel’s newly outlined strategy ST28 is comprehensive and well-targeted, focusing on expansion, managing financial strength and restructuring of assets. S$8 billion dollars is set aside for investment and debt management. This is about 50% of the FY2024’s reported operating revenue which justifies the rally. Furthermore, planned capital expenditure of S$2.8 billion, which translates to 20% of current operating revenue, provides a glimpse of the management’s long term vision. Together, this initiatives suggest a bold restructuring and steering of the development direction of Singtel, which has been positively received by investors.

Q1 2025 Earnings

Singtel’s most recent earnings were encouraging, with net profit growing 42.9% to S$690 million, despite a 2.1% decline in operating revenue to S$3,413 million. Its EBITDA margin also increased by more than 2% to 28.6% showing an increasing efficiency in the business operations.

Within its operations, Optus and Singtel Singapore recorded a drop in revenue while NCS and Digital InfraCo recorded an increase in revenue as shown below. Optus is a subsidiary under Singtel that operates in Australia as a telecommunications company. Singtel Singapore is the portion of business that operates in Singapore and contributes 27% of overall revenue. NCS, is a business segment that focuses on providing digital, cloud services across Asia in sectors like government, healthcare, finance. Digital InfraCo is Singtel’s standalone infrastructure business that has key assets like regional data centres, submarine cables, satellite services and paragon platforms.

Optus

Optus’ mobile service revenue rose 4.7%, driven by price increases in postpaid plans and a higher prepaid customer base. However, overall operating revenue declined by 3.2% due to lower ICT and project-based satellite revenues. With improved mobile performance and effective cost management, EBITDA increased 4.6%.

EBIT surged 58%, reflecting a reduction in depreciation and amortization charges from a lower asset base. In June 2024, Optus acquired 900 MHz spectrum for S$1.3 billion (A$1.5 billion).

Singtel Singapore

Singtel Singapore’s operating revenue remained stable amid a highly competitive market. Mobile service revenue rose 6.8%, driven by roaming growth and Internet of Things (IoT) connectivity, particularly from connected cars. However, these gains were offset by structural declines in legacy carriage services, such as fixed voice, data, and Internet services.

Operating expenses fell due to lower direct cost of sales and reduced manpower costs from a smaller average headcount. As a result, EBITDA grew 3.5%, while EBIT remained stable, affected by higher depreciation from IT and network investments.

NCS

NCS’ operating revenue grew 3.8%, fueled by growth in its Gov+ and Telco+ businesses. With higher revenue and continued cost optimization, EBITDA rose 13%, and EBIT surged 28%.

The financial year began strongly for NCS, with bookings of S$788 million from a pipeline of projects across multiple sectors.

Digital InfraCo

Digital InfraCo’s revenue increased 5.8%, driven mainly by Nxera, thanks to higher customer reservation fees, utility pass-through, and price uplifts. However, these gains were partly offset by declining fees from project-based satellite deployments.

EBITDA and EBIT declined by 13% and 32%, respectively, due to lower satellite fees during Nxera and Paragon’s expansionary phase. In July 2024, Nxera broke ground on its new sustainable, hyper-connected AI-ready data center in Johor, Malaysia, marking a strategic entry into a new market.

Overall, these results mark a significant turnaround from its FY 2024 which saw net profit down 64% due to a huge loss from non-cash impairment charges. Businesses like NCS and Digital InfraCo maintained their growth momentum. While Optus and Singtel Singapore recorded losses, it is clear that they are becoming more efficient through increased EBITDA and EBIT numbers. We believe that they can turn positive as the business continues its restructuring through its ST28 plans to stimulate growth.

Regional Associates performances

Singtel’s regional associates recorded an overall drop in pre-tax contributions by 3% mainly due to a fall in contributions by Bharti telecom and Telkomsel by 13.8% and 8.8% respectively. Singtel holds substantial stakes in Indonesia’s Telkomsel, Philippines’ Globe Telecom, Thailand’s AIS & Intouch and India’s Airtel.

AIS, Intouch and Globe recorded teen double digit increases, a commendable performance likely to continue, driven by increased data center development across Southeast Asia.

Singtel’s regional associates have largely enjoyed strong growth, with the exception of Telkomsel (Telkom Indonesia). This is because Telkom Indonesia has a losing investment in GoTo. We expect that an increase in data centre installation and a shift towards digitalisation will lead to an increase in value for these telcos. There is also a trend of shifting data centre buildings from Singapore to its neighbouring countries, which will further benefit these regional associates of Singtel.

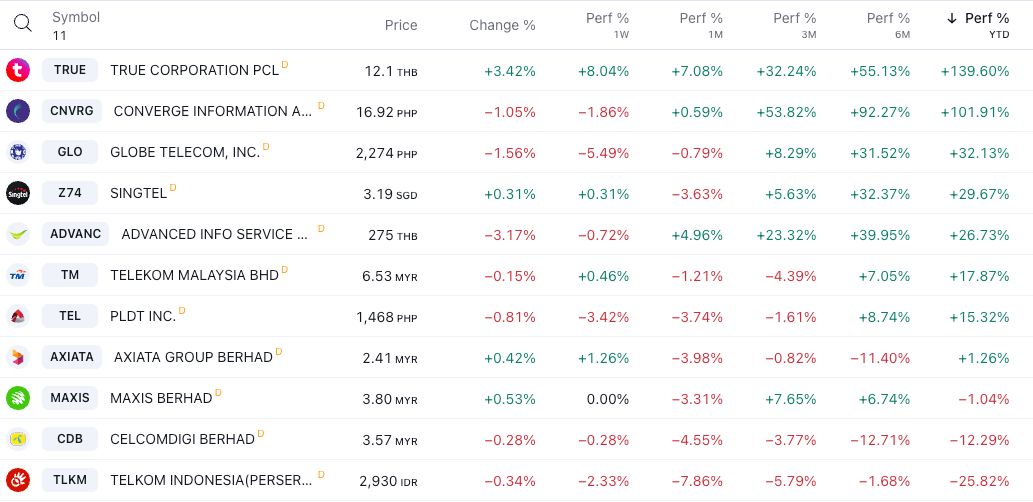

Other regional telcos like True Corporation, Converge Information have also presented strong growth, especially in the Thailand and Philippines market where AIS, Intouch and Globe operate. We believe the strong growth in some of them is due to their critical investments in data centre facilities. For example, True Internet Data Centre is investing over 10 billion baht to expand its data centres. Similarly, Singtel and Converge ICT are also increasing their investments in data centre facilities. On the other hand, Globe announced its investment in Mynt, parent company of digital cashless payment ecosystem GCash. These shows a variety of strategic investments that will boost the telcos’ values. There seems to be a strong correlation between strategic data centres expansions and the growth potential of these telcos, fueling their explosive growth.

However, there are some that are shown below that remain in the red YTD. While they may have invested in data centres too, their investments may be more of a bane than a boon. Telkom Indonesia has underperforming investments in GoTo technology company, while Axiata have investments in data centres in Bangladesh with uncertain future development due to local unrest. These factors may be hindering the performance of these regional telcos.

What we believe catalyzed the 30% upward move in Singtel

Singtel28 is an initiative that plans to enhance customer experiences and drive the business’s growth. Through this initiative, Singtel seeks to increase investment in 5G technology, establish strong 5G leadership in Singapore and provide 5G coverage in Australia through Optus. The funding of these programmes are provided through freeing up S$8 billion from assets such as stakes in Indara, Airtel and Nxera under its capital recycling strategy. One of the important aspects of this strategy was the reduction of Singtel’s stake in Comcentre from 100% to 51%, which provides dry powder for Singtel to invest in higher growth potential areas and its core businesses rather than real estate. Through this initiative, the increasing investment in data centres would be an important growth narrative that Singtel can ride on.

Singtel is also scaling up in the ICT and data centre space by expanding NCS and Nxera. NCS aims to improve its margins while scaling up the global delivery network and investing in AI and tech to benefit its clients. On the other hand, Nxera plans to expand its operational data center capacity in the region from 62MW to 155MW by building 3 next generation AI-ready data centre in Singapore, Thailand and Indonesia.

Another positive development is its divestment of non-core digital businesses Amobee and Trustware which effectively removes S$200 million in annual EBIT losses. Singtel also continues to gain as its regional associates expands, with the combination of IndiHome and Telkomsel and the integration of 3BB and AIS.

Lastly the business is focusing on maximising shareholder value through increased dividend payouts. This came in the form of a new value realisation dividend of 3 to 6 cents per share per annum, in addition to the core dividend, which had its payout range raised to 70% and 90% of underlying net profit last November.

Through these multi pronged approaches, we see possible growth of the business fundamentally. Furthermore, as global interest rates are set to decrease, the regional currencies are set to be buoyed and have weaker devaluating pressure due to the likely weakening of the USD. This will reduce the impact on the various regional associates and subsidiaries of Singtel when accounting their contributions. This is especially crucial for the Bharti Airtel Group’s Africa business which has accounted for a 20% drop in contributions in Q1 2025 due to weakening of Nigerian Naira and Malawi Kwacha.

Singtel is also a financially stable business. For FY2024, it has lowered its net debt by 7% to S$7.78 billion and almost 90% of its debt is locked in at fixed rates, ensuring low uncertainties in repayment of its debt under current uncertain macroeconomic situation. Furthermore, its S$8 billion raised through restructuring of its assets are used to invest and repay debt to maintain the strong solvency of Singtel.

Singtel aims to boost EBIT growth rate to low double digits through ST28. This growth projection includes a planned S$2.8 billion in capital expenditure for 5G network installations and cyber security and digital transformation initiatives across Singapore and Australia. This means that Singtel is expecting a further increase in efficiency in its operations, which will be beneficial to increase its margins amidst the competitive telco landscape in Singapore and Australia. Overall, we view these developments positively, as they are important in solidifying Singtel’s local and regional market leadership.

Valuation and Conclusion

Currently, Singtel’s valuations are as follows (current multiples vs 5-year average) :

- ROA: 1.71 vs 2.74

- ROE: 3.12 vs 4.87

- Dividend yield: 3.50 vs 3.94

- FCF yield: 4.46 vs 5.85

These metrics indicate that Singtel has much room to recover compared to its previous operating performance levels. We see that this is possible due to various opportunities present in the region. Multinational corporations are increasingly building data centres across the SEA region. Singapore is trying to position itself as an attractive destination for these businesses in competition with its lower-cost neighbours. There have been talks of building small modular reactors to sustain the energy demand.

Next, SEA is an important market for gaming. With China’s gradually relaxaing its gaming regulations, companies like Tencent and NetEase will seek to expand its gaming audience across the region, which will provide ample market opportunities for Telcos. Furthermore, China’s digital Belt and Road Initiative will also be a driver bringing up the demand for data centres, further stimulating growth of telcos as various ecommerce businesses expands internationally, bringing about online payment and generating online data through sales, live commerce, etc. This is a non-exhaustive list of opportunities available and all these services operate on the fundamental support that telcos can provide.

Singtel’s YTD rally of 30% represents a S$12.2 billion increase in market cap, which prices in its various strategic manoeuvres outlined earlier. However, we believe that this is not the end of its rally, as its yearly overall revenue growth remains negative. We foresee a turnaround would serve as a catalyst for the stock to continue its momentum and return to operation metrics similar to its peak or beyond.

p.s. if you want to learn how to analyse and find the best stocks to buy, Alvin shares our strategy at this live webinar.